Exacta Staking Plans: Flat Stake, Proportional and Bankroll-Based Approaches

I lost 23 consecutive exacta bets in the autumn of 2019. Twenty-three. The losing streak lasted six weeks, covered four different racecourses, and included several combinations that missed by a neck or a short head. What kept me solvent was not the quality of my selections – clearly those were questionable that month – but the staking plan that kept each bet to 1% of my rolling bankroll. When the 24th bet landed an exacta dividend of 287 to a 1 unit, the recovery was immediate. Without a staking discipline, that streak would have emptied my account long before the winner arrived.

Flat Staking and Its Limits

Every punter I know started with flat staking. You pick a number – two quid, a fiver, ten pounds – and that is your stake on every bet. The appeal is obvious: no maths, no adjustment, no thinking about the bet beyond the selections. For exacta betting, flat staking means your unit stake stays constant regardless of the race, the field size, or the expected dividend.

Flat staking works when your edge is consistent and your bankroll is large relative to your stakes. If you are betting 1 units on exactas and your bankroll is 500, you have 500 units of runway. Even a brutal losing streak struggles to wipe that out. The problem arises when the edge varies between races. A 6-runner Group 1 and a 20-runner heritage handicap present wildly different exacta opportunities, but flat staking treats them identically. You commit the same capital to a low-dividend, high-probability bet as you do to a high-dividend, low-probability one.

I used flat staking exclusively for my first three years of pool betting. My results were modestly profitable but lumpy – long flat stretches interrupted by occasional big dividends. The mathematical profile of exacta returns, where the average dividend across UK turf flat racing sits around 102.44 per 1 unit but the median is far lower, means that flat staking amplifies the variance without compensating for the structural unevenness of returns.

Proportional Staking by Bankroll

The idea behind proportional staking is elegant: bet a fixed percentage of your current bankroll on each wager. Your stakes grow when you win and shrink when you lose, creating a self-correcting mechanism that prevents ruin.

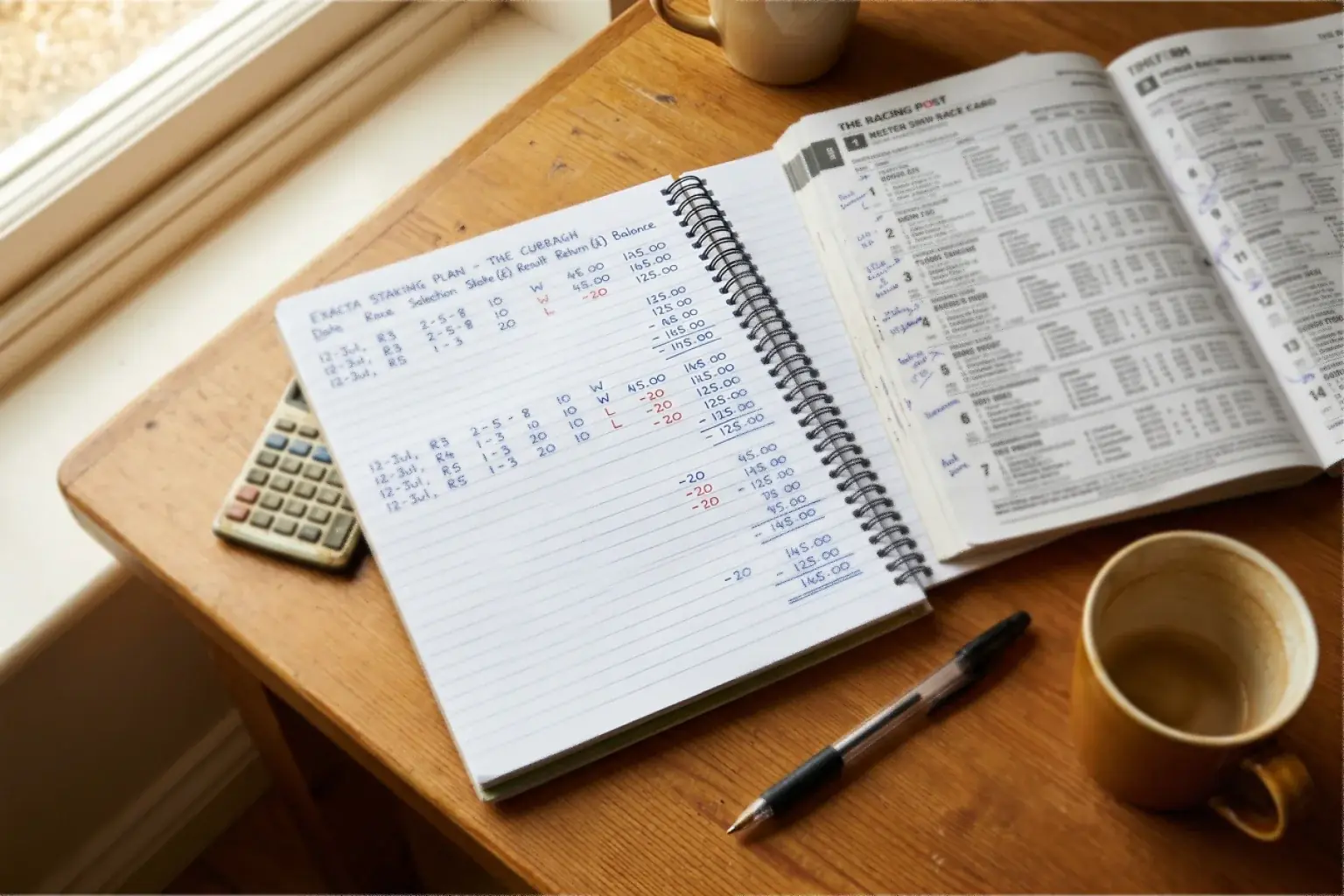

For exacta betting, I use 1.5% of my rolling bankroll as the total cost of each bet – not the unit stake, but the total outlay including all combinations. If my bankroll is 1,000, my total exacta spend on a single race is 15. If I am playing a 3×5 part wheel, that 15 divided by 15 combinations gives a unit stake of 1. If my bankroll drops to 600 after a losing spell, the same structure costs 9 and the unit stake drops to 60p.

This approach has two advantages that flat staking lacks. First, it makes ruin theoretically impossible – as your bankroll shrinks, so do your stakes, creating a Zeno’s paradox of losing where you can never quite reach zero. Second, it automatically increases your exposure during winning periods, letting you compound returns when your selections are running well. The compounding effect is particularly powerful with exacta betting because a single large dividend can shift your bankroll substantially, and the subsequent larger stakes multiply the benefit of your next winner.

The disadvantage is psychological. Watching your stakes shrink during a losing run feels like retreat, and it requires discipline to resist the urge to override the formula and chase losses with a larger bet. The formula does not care about your feelings – it only cares about the bankroll number.

Adjusting Stake by Expected Dividend

Here is where exacta staking gets interesting. Not all exacta opportunities are equal, and a smart staking plan reflects the expected dividend range of each bet.

Favourites win 30-35% of UK races overall, and in small fields that percentage climbs higher. An exacta involving two market leaders in a 7-runner race has a relatively high probability of landing but will pay a modest dividend. An exacta involving two unconsidered horses in a 20-runner handicap has a low probability but enormous dividend potential. Staking the same amount on both is a missed opportunity.

My approach is to categorise each exacta bet into three tiers based on expected dividend. Low-dividend bets – those where I expect the exacta to pay between 10 and 50 – get a smaller unit stake because the return does not compensate for heavy investment. Mid-range bets – expected dividends of 50 to 200 – get my standard unit. High-dividend bets – where I am targeting outsider combinations that could pay 200 or more – get a slightly lower unit but wider coverage, meaning more combinations at a smaller unit stake.

This creates a portfolio effect across a day’s betting. The low-dividend bets provide frequent small returns that sustain the bankroll. The mid-range bets are the core of the strategy, balancing probability and payout. The high-dividend bets are the tail risk plays, where one hit every 15-20 attempts can transform a month’s figures. The total capital deployed stays within the proportional bankroll limit, but the distribution across bet types is weighted by expected return rather than treated as identical.

Tracking and Adjusting Over Time

A staking plan without records is a staking plan without feedback. I maintain a spreadsheet that logs every exacta bet with the race details, combination structure, unit stake, total cost, result, and dividend. After every 100 bets, I review three metrics: strike rate, average winning dividend, and return on investment.

The strike rate tells me whether my selection process is working. For structured exacta bets using part-wheels and bankers, I target a strike rate of 8-12%, meaning one winner in roughly every ten bets. Below 6% over a sustained period suggests my selection criteria need tightening. Above 15% suggests I am being too conservative and missing higher-dividend opportunities.

The average winning dividend tells me whether my winners are paying enough to offset the losers. With a 10% strike rate, I need an average dividend of at least 12 per 1 unit to break even after accounting for the nine losing bets. My actual target is an average dividend north of 15, which provides a comfortable margin and accounts for the 25% pool deduction that is already baked into the declared figure.

Return on investment is the bottom line: total returns divided by total stakes. Anything above 100% means profit. I aim for 115-120% ROI across a season, which sounds modest but compounds meaningfully over hundreds of bets. The key insight from tracking is that staking adjustments – shifting from flat to proportional, tiering by expected dividend – improved my ROI by roughly 8 percentage points without changing my selection process at all. The same horses, the same races, the same combinations. The only difference was how much I put on each one, and that difference was worth real money over the course of a season of exacta strategy.

What percentage of bankroll should I stake on each exacta bet?

A common range is 1-2% of your total bankroll as the maximum total cost per race. This means the combined cost of all combinations in your exacta bet – not the unit stake – stays within that percentage. At 1.5% with a 1,000 bankroll, your total exacta outlay per race is 15, which might translate to a 1 unit stake across 15 combinations or a 50p unit stake across 30 combinations.

Is flat staking or proportional staking better for exacta betting?

Proportional staking is more resilient because it prevents ruin during losing streaks and compounds gains during winning periods. Flat staking is simpler and works adequately with a large bankroll relative to stakes. For exacta betting specifically, where dividends are highly variable and losing streaks can be extended, proportional staking offers a structural advantage by keeping your exposure calibrated to your current bankroll.

Elaborado por el equipo de «Horse Racing Exacta bet».